Flexible packaging paper is evolving into a high-performance, recyclable solution, replacing plastics through advanced coatings, strong barrier properties, and growing regulatory support.

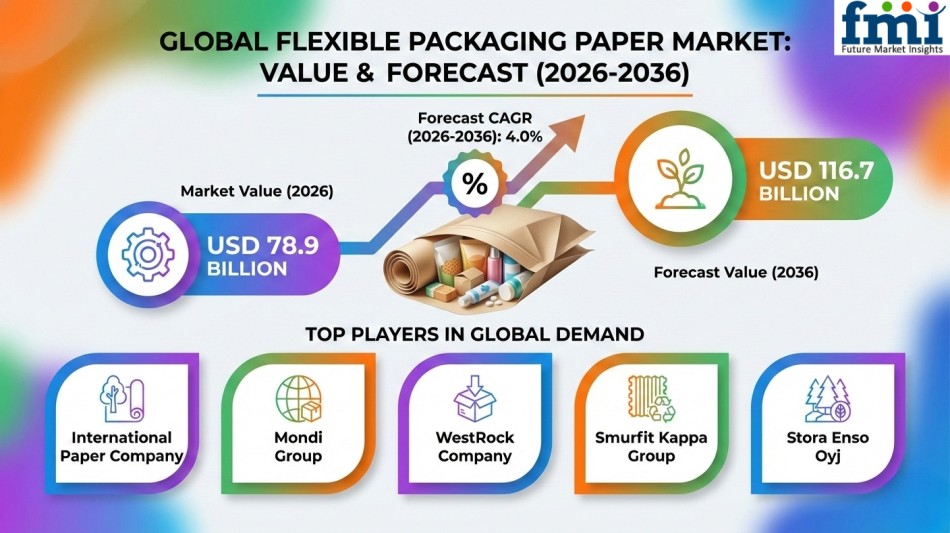

NEWARK, DELAWARE / ACCESS Newswire / February 24, 2026 / The global flexible packaging paper market is entering a new phase of steady, performance-driven expansion. Valued at USD 78.9 billion in 2026, the market is projected to reach USD 116.7 billion by 2036, growing at a CAGR of 4.0%. This growth reflects a fundamental shift in packaging priorities, where flexible packaging paper is no longer positioned merely as a substitute for plastic, but as a core structural component of modern packaging systems.

According to a comprehensive strategic outlook from Future Market Insights (FMI), the category has evolved into a key growth engine within the broader paper industry, supported by regulatory clarity, brand commitments to sustainability, and ongoing material innovation. Demand has moved decisively toward high-performance paper formats that combine recyclability with functional equivalence to traditional plastic solutions.

Flexible Packaging Paper Market Metrics and Growth Outlook

The flexible packaging paper market reflects stable, value-driven growth supported by evolving industry requirements.

Flexible Packaging Paper Market Snapshot (2026-2036):

-

Current Market Value (2026): USD 78.9 Billion

-

Projected Market Value (2036): USD 116.7 Billion

-

Global Growth Rate (CAGR): 4.0%

-

Leading Material Type: Kraft Paper

-

Fastest-Growing Countries: India, USA, Germany, Brazil, China

Discover Growth Opportunities in the Market – Get Your Sample Report Now: https://www.futuremarketinsights.com/reports/sample/rep-gb-7946

The Structural Shift: From Substitution to Performance Engineering

The competitive landscape of flexible packaging paper is being reshaped by a transition from basic substitution strategies to performance-driven engineering. Over the past two to three years, manufacturers have prioritized barrier functionality, grease resistance, sealability, and machinability as essential product attributes.

The market has shifted away from traditional commodity kraft paper toward engineered paper solutions designed for pouching, wrapping, sachets, and mailers. These formats are evaluated not only for sustainability, but also for operational performance metrics such as line speed, shelf life, conversion efficiency, and recyclability outcomes.

Between 2023 and 2025, the industry underwent a reset phase marked by cost volatility, energy disruptions, and inventory corrections. By 2024, both production and consumption rebounded, with packaging grades leading the recovery. Flexible and wrapping paper formats outpaced graphic and hygiene grades, confirming a long-term transition in demand patterns.

Regulation as a Market Catalyst

Regulatory developments are accelerating the adoption of flexible packaging paper globally. A key turning point comes with the implementation of the EU Packaging and Packaging Waste Regulation, Regulation (EU) 2025/40, adopted in 2024 and entering into force in 2025, with mandatory application beginning August 12, 2026.

As a regulation rather than a directive, it applies uniformly across EU member states without requiring national transposition. These rules explicitly favor recyclable-by-design packaging structures and discourage complex multi-material formats.

This regulatory clarity is compressing product development timelines and encouraging early specification locking by brand owners. Packaging formats that meet European compliance standards are increasingly becoming global benchmarks, accelerating the adoption of recyclable paper-based solutions across international markets.

Segment Spotlight: Material and Product Dynamics

Material Leadership

Kraft paper continues to dominate the market, accounting for 52.1% of total demand, supported by its widespread use in food packaging, retail bags, and industrial applications. Greaseproof paper holds 23.7%, driven by food service and bakery packaging requirements, while parchment paper accounts for 15.2%, primarily used in cooking and baking applications. Other materials contribute 9.0%, serving niche and specialized use cases.

Material selection is increasingly influenced by moisture resistance, grease barrier performance, and recyclability compatibility, reflecting the growing importance of application-specific engineering.

Product Segmentation

Food packaging remains the largest product segment, representing 48.3% of the market, driven by the need for food-safe materials with reliable barrier protection. Retail bags account for 28.4%, supporting consumer convenience and branding requirements, while industrial wrapping holds 14.6%, focusing on durability and protective performance. Specialty packaging contributes 8.7%, catering to decorative and niche applications.

The dominance of food packaging underscores the critical role of flexible paper in maintaining product integrity while meeting regulatory and sustainability standards.

Regional Powerhouses: Global Growth Patterns

While demand for flexible packaging paper is global, growth rates vary significantly by region, reflecting differences in manufacturing capacity, food processing activity, and regulatory frameworks.

Flexible Packaging Paper Market by Country

|

Country |

CAGR (2026-2036) |

|

India |

5.8% |

|

USA |

4.5% |

|

Brazil |

4.7% |

|

China |

4.3% |

|

Germany |

4.1% |

Global Trade Dynamics: Export and Import Trends

Flexible packaging paper is produced and traded across a global network of manufacturing and consumption hubs. Major exporting regions include North America, Europe, and Asia, where advanced production capabilities and coating technologies support the manufacture of food-grade and specialty packaging materials.

Germany is recognized as a leading exporter, supported by its advanced manufacturing infrastructure and precision coating technologies. The United States and Finland also play significant roles in supplying global markets, while China contributes through large-scale, cost-effective production capabilities. Additional exports originate from European and Nordic manufacturing hubs.

On the demand side, importing countries are characterized by expanding food processing and consumer goods industries. India is among the leading importers, driven by the need to support domestic packaging requirements in growing retail and food sectors. The United States and Brazil also import specialized packaging materials, while China and Germany serve as key markets for premium and high-performance packaging solutions.

Dynamics of the Decade: Recycling, Cost, and Performance

The flexible packaging paper market is being shaped by several key dynamics that will define its trajectory through 2036:

-

Recycling and Circular Economy Requirements: Recyclability has become a central factor in packaging selection. Manufacturers are prioritizing fiber recovery rates, recycling compatibility, and circular economy compliance. Paper-based packaging is increasingly favored for its ability to integrate into existing recycling systems while maintaining performance standards.

-

Cost Constraints and Material Selection: Adoption is influenced by fluctuations in pulp pricing, coating material availability, and regional recycling infrastructure. Manufacturers must balance barrier performance, printability, and cost efficiency, leading to more complex procurement and material selection strategies.

-

Performance-Driven Packaging Decisions: End-users are evaluating packaging based on barrier properties, machinability, forming capabilities, and compatibility with existing filling and printing systems. Performance under storage and distribution conditions remains a critical consideration in product selection.

Competitive Landscape: Scale Meets Sustainability

The competitive environment is defined by global paper and forest product companies expanding their portfolios into sustainable packaging solutions. Leading players are leveraging production scale, innovation, and recycling capabilities to strengthen their market positions.

Key companies operating in the flexible packaging paper market include International Paper Company, Mondi Group, WestRock Company, Smurfit Kappa Group, Stora Enso Oyj, Georgia-Pacific LLC, Nine Dragons Paper Holdings Limited, Sappi Limited, UPM-Kymmene Corporation, and Nippon Paper Industries Co., Ltd.

These companies are investing in advanced fiber technologies, barrier coatings, and recycling systems to meet evolving regulatory requirements and customer expectations. Strategies include expanding production capacity, enhancing product performance, and developing recyclable packaging solutions tailored to food, retail, and industrial applications.

For an in-depth analysis of evolving formulation trends and to access the complete strategic outlook for the Flexible Packaging Paper Market through 2036, visit the official report page at: https://www.futuremarketinsights.com/reports/flexible-packaging-paper-market

Related Reports:

-

Paper Packaging Tapes Market – https://www.futuremarketinsights.com/reports/paper-packaging-tapes-market

-

Paper Packaging Market – https://www.futuremarketinsights.com/reports/paper-packaging-market

-

Flexible Packaging Machinery Market – https://www.futuremarketinsights.com/reports/flexible-packaging-machinery-market

-

Paperboard Packaging Market – https://www.futuremarketinsights.com/reports/paperboard-packaging-market

-

Flexible Plastic Packaging Market – https://www.futuremarketinsights.com/reports/flexible-plastic-packaging-market

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading provider of market intelligence and consulting services, serving clients in over 150 countries. Headquartered in Delaware, USA, with a global delivery center in India and offices in the UK and UAE, FMI delivers actionable insights to businesses across industries including automotive, technology, consumer products, manufacturing, energy, and chemicals.

An ESOMAR-certified research organization, FMI provides custom and syndicated market reports and consulting services, supporting both Fortune 1,000 companies and SMEs. Its team of 300+ experienced analysts ensures credible, data-driven insights to help clients navigate global markets and identify growth opportunities.

For Press & Corporate Inquiries

Rahul Singh

AVP – Marketing and Growth Strategy

Future Market Insights, Inc.

+91 8600020075

For Sales – sales@futuremarketinsights.com

For Media – Rahul.singh@futuremarketinsights.com

For web – https://www.futuremarketinsights.com/

SOURCE: Future Market Insights, Inc.

View the original press release on ACCESS Newswire