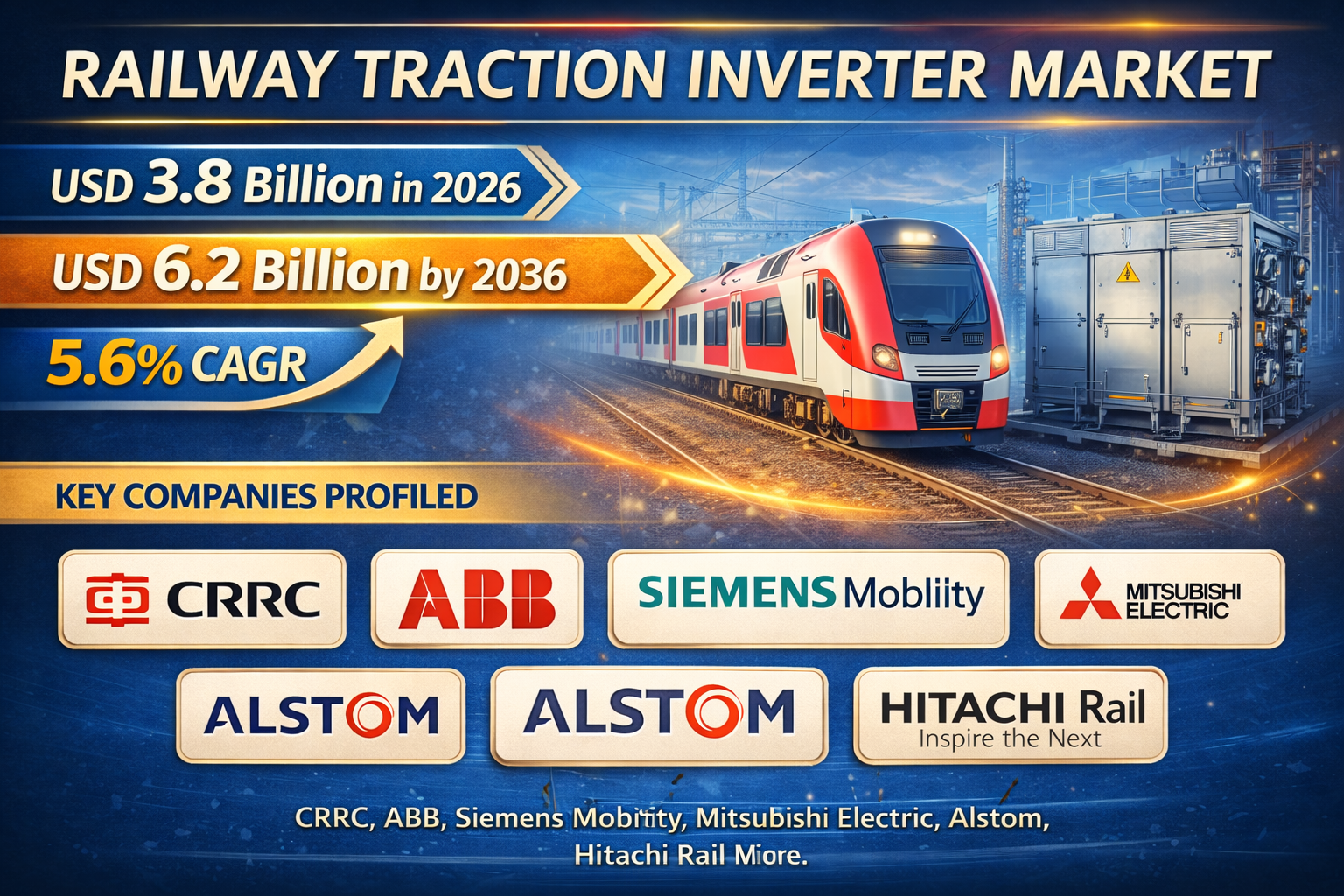

The global railway traction inverter sector is on track to achieve a valuation of USD 6.2 bn by 2036, accelerating from USD 3.8 bn in 2026 at a CAGR of 5.6%.

NEW YORK, DE, UNITED STATES, February 13, 2026 /EINPresswire.com/ — The global Railway Traction Inverter Market is projected to expand from USD 3.8 billion in 2026 to USD 6.2 billion by 2036, registering a 5.6% CAGR over the forecast period. Growth is structurally underpinned by railway electrification programs, rolling stock replacement cycles, and migration toward silicon carbide (SiC) power electronics platforms. As electrified railway networks surpassed 390,000 km globally, according to UIC reporting cited in the study, rolling stock OEMs are scaling traction power electronics production. The shift from IGBT-based systems to SiC MOSFET platforms is redefining inverter efficiency, compactness, and reliability across high-speed rail, metro, and electric locomotive applications.

Direct Answers

Market size in 2026? USD 3.8 billion

Market size in 2036? USD 6.2 billion

Projected CAGR (2026–2036)? 5.6%

Industry Size (2026) – alternate dataset? USD 5.1 Billion

Industry Value (2036) – alternate dataset? USD 8.8 Billion

Largest country share? China

Leading technology segment (2025)? SiC – 30.2%

Leading train type (2025)? Metro – 32.4%

Market Momentum (YoY Path)

The Railway Traction Inverter Market reflects steady compounding:

2026: USD 3.8 billion

H1 2026 growth: 5.4%

H2 2026 growth: 5.6%

2030: Growth driven by electrification acceleration

H1 2036 CAGR: 5.5%

H2 2036 CAGR: 5.7%

2036: USD 6.2 billion

The bi-annual progression indicates incremental basis-point improvements between first and second halves, signaling stable capital deployment across traction electronics programs.

Request For Sample Report | Customize Report | Purchase Full Report – https://www.futuremarketinsights.com/reports/sample/rep-gb-10536

Why the Market is Growing

The Railway Traction Inverter Market is expanding due to global railway electrification and replacement of diesel-powered fleets. Governments are prioritizing sustainable transport systems and reducing carbon intensity in rail networks. Technological migration toward SiC MOSFET-based designs enhances power density, reduces weight, and lowers energy consumption per train-kilometer. High-speed rail expansion and metro system investments are reinforcing inverter demand. Additionally, local manufacturing mandates in countries such as Australia, India, and Turkey are reshaping procurement frameworks.

Segment Spotlight

Technology Type: SiC Leads at 30.2%: SiC-based inverters account for 30.2% share in 2025, driven by superior efficiency, reduced switching losses, compact form factors, and improved thermal performance. The migration from silicon IGBT to SiC MOSFET designs enables higher power density and lower maintenance. China and Europe are deploying SiC platforms in high-speed rail corridors to improve operational efficiency and reduce lifecycle energy costs.

Train Type: Metro Dominates at 32.4%: Metro systems represent 32.4% share in 2025, reflecting rapid urbanization and demand for reliable public transit. Regenerative braking compatibility and energy recovery integration make traction inverters central to metro efficiency strategies. Countries such as India, Indonesia, and Vietnam are expanding metro infrastructure, strengthening inverter procurement pipelines.

Market Definition

The Railway Traction Inverter Market includes revenue from power electronic inverter systems converting DC to AC for traction motors in electric locomotives, EMUs, metros, and trams. Included are IGBT and SiC MOSFET traction inverters, auxiliary converters integrated with traction, and battery-traction hybrid platforms. Excluded are standalone traction motors, signaling power supplies, diesel-electric alternator systems, and HVAC inverters outside the traction chain.

Drivers, Opportunities, Trends, Challenges

Drivers: Global electrification programs, high-speed rail investments, and metro network expansion are primary growth catalysts. UIC data showing more than 390,000 km of electrified rail underpins long-term inverter demand.

Opportunities: SiC MOSFET adoption, PMSM integration in high-speed rail, and local production mandates create procurement-driven opportunities. Public-private partnerships and government incentives further reinforce capital inflows.

Trends: Shift from IGBT to SiC, modular inverter architectures, lighter materials, and localized manufacturing are shaping competitive differentiation. PMSM traction adoption in high-speed rail is redefining performance benchmarks.

Challenges: Balancing global technology platforms with domestic content mandates complicates procurement. Retooling manufacturing for SiC modules and maintaining thermo-mechanical reliability present operational hurdles.

Competitive Landscape

The Railway Traction Inverter Market demonstrates moderate concentration. Tier-1 companies account for approximately 55–60% of total market share, with product revenues exceeding USD 500 million. Tier-2 players contribute roughly 40–45%.

Leading companies include Schneider Electric, CRRC, Wabtec, General Electric, Toshiba, Mitsubishi Electric, ABB, Siemens, Alstom, and Hitachi.

Strategic moves include CRRC’s January 2025 unveiling of the CR450 EMU prototype with high-torque PMSM direct-drive traction motor and upgraded inverter. In December 2025, ABB inaugurated a 5,000-square-meter Traction Centre of Excellence in Australia for local converter production. Mitsubishi Electric deployed SiC module-based traction systems in European applications.

Competition centers on SiC integration, modular scalability, localized manufacturing, and reliability engineering.

Scope of the Report

Quantitative Units (2026): USD 5.1 Billion

Product Type:

IGBT Traction Inverters

SiC MOSFET Inverters

Hybrid Systems

Application:

High-Speed Rail

Commuter EMU

Metro

Light Rail

Locomotives

Regions Covered: North America, Europe, Asia Pacific, Latin America, Middle East and Africa

Key Companies Profiled: CRRC, ABB, Siemens Mobility, Mitsubishi Electric, Alstom, Hitachi Rail

Why FMI: https://www.futuremarketinsights.com/why-fmi

Have a Look at Related Research Reports on the Packaging Domain:

Railway Telematics Market: https://www.futuremarketinsights.com/reports/railway-telematics-market

Railway System Market: https://www.futuremarketinsights.com/reports/railway-system-market

Railway Communication Equipment Market: https://www.futuremarketinsights.com/reports/railway-communication-equipment-market

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

Sudip Saha

Future Market Insights Inc.

+1 347-918-3531

email us here

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()